Blue View

Project Blue’s free critical materials analysis - commentary, insight and video in one place.

Refine your search

Filter by

Spotlight Analysis

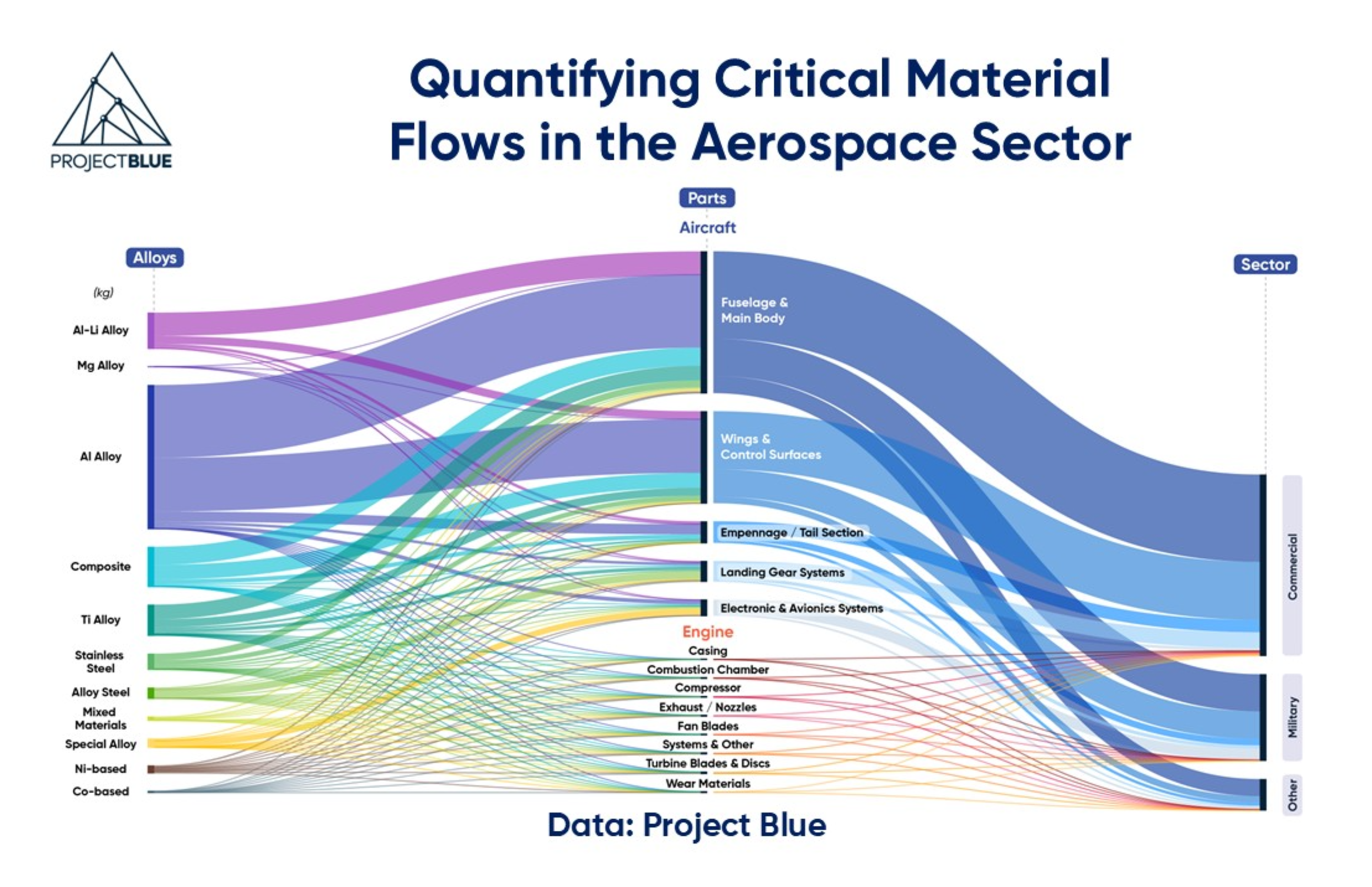

Quantifying critical material flows in the aerospace sector

Follow On

Subscribe nowLoading articles...